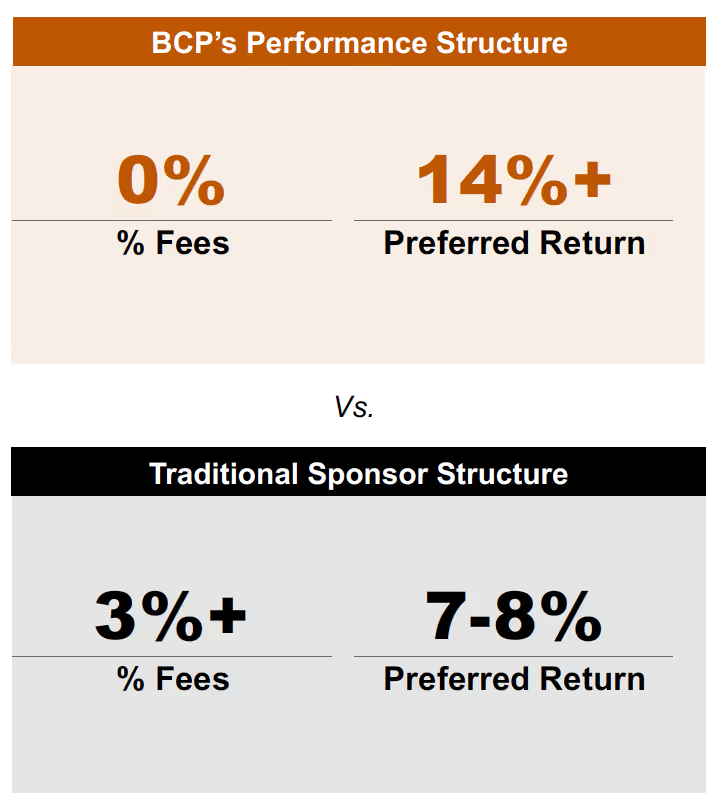

BCP’s Performance-Based Structure

Buchanan Capital Partners' performance-based structure has two key components that differentiates us from traditional sponsors : Fees and Preferred Return

Fees

BCP charges NO fees and only profits after a project has surpassed the investor’s IRR expectation. BCP’s sole motivation is project performance. We are driven by quality over quantity.

Traditional sponsors charge numerous fees (including acquisition, asset management, loan guaranty, disposition, etc.) that provide guaranteed income to their in-house brokerage, property management, or construction management divisions. Fee-driven sponsors profit by doing the deal, even on underperforming investments which can incentivize a risk-forward, quantity over quality mentality.

Preferred Return

BCP structures high IRR preferred returns (approx. +/- 65% higher than traditional preferred return hurdles) where the investor’s return is clearly defined, and the investors are paid out first.

Our high IRR is based on Risk / Return metrics. Traditional sponsors have a lower initial preferred return with a multi-tier waterfall, where sponsors share in the profit of a deal much earlier.

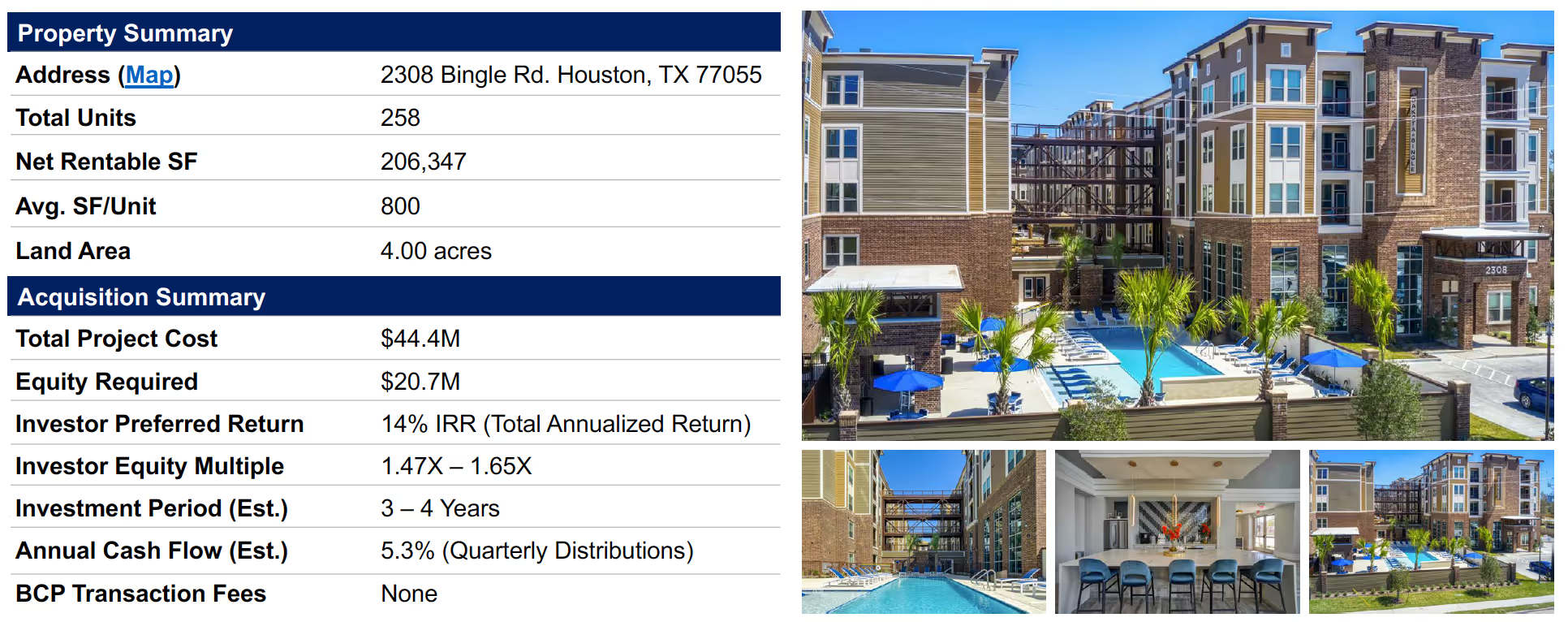

To highlight the comparison between BCP’s and Traditional Sponsors structures, we’ve used a recent acquisition to compare the approaches.

Belle Spring Branch (formerly “Dakota At Bingle”) was an off-market BCP acquisition of a fully-stabilized 258-unit, 5-story midrise apartment community in the rapidly developing submarket of Spring Branch East in Houston, TX. BCP closed on the property in November of 2023.

Using Belle Spring Branch as a case study, it is evident that traditional sponsor fees adversely impact investment performance for two main reasons: Total Equity Required and Cash Flow

Increased Equity Check Size

Since traditional sponsors charge an acquisition fee, they need to raise more equity to close the transaction.

Takeaway: A traditional structure requires an additional $648,750, or 3.1%, in equity, all of which is paid as a fee to the sponsor at closing.

Decreased Investor Cash Flow

The standard asset management fees charged by traditional sponsors are paid from investor cash flow. The table below demonstrates the impact that a standard asset management fee over a 3-year hold has on distributable cash.

Takeaway: A traditional structure decreases distributable cash, reducing the annual distributions to investors and overall return on equity.

Result: A traditional sponsor makes $961,560 in fees regardless of the investor return performance.

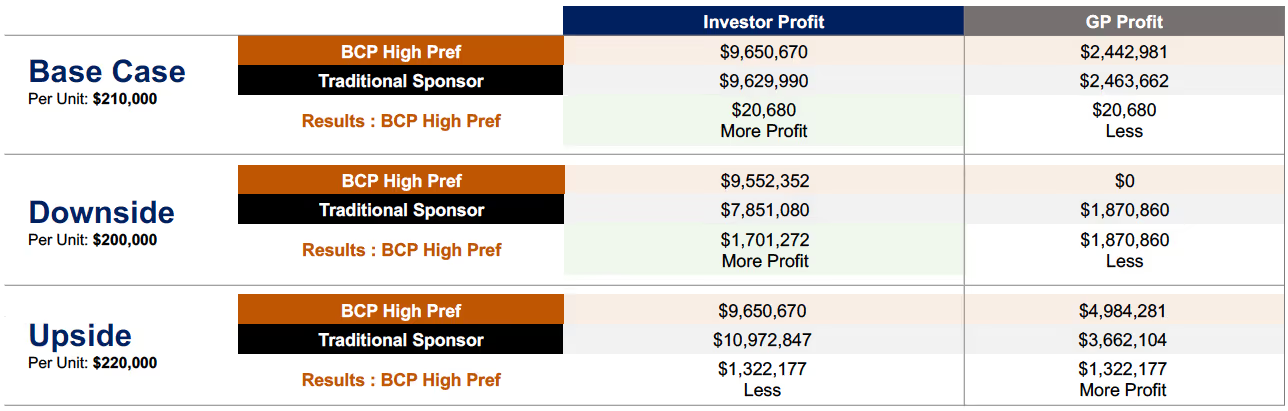

Diving further into this comparison, we compare investor returns across multiple sale scenarios to demonstrate the benefits to our investors of BCP's 100% performance-based structure.

Key takeaways from comparison:

- BCP investors make more profit in all but the pro forma beating upside scenario

- BCP's 14% IRR yields more investor profit than a typical, fee-loaded 14% IRR

- BCP's profit is entirely dependent on exceeding investor return targets

Using the per unit sales price as the only changing variable, the following table highlights investor and GP profit across three scenarios: Base Case, Downside, and Upside

Final Conclusions

Fees

Before an investment has been realized, traditional sponsors have already made money through their transaction fees. Because of that, many traditional sponsors are incentivized to do more volume – the promote is just a cherry on top of the fee stream revenue.

Promote

With a typical multi-tier promote structure, the traditional sponsor takes an early and higher share of the upside after a lower preferred return. Conversely, BCP only makes money after its higher preferred return threshold is achieved.

Downside Case

If a deal underperforms, investor’s profit is considerably higher with BCP’s Performance-Based structure because BCP receives zero compensation until our investors receive their clearly defined return (no fee-load, 100% back-end motivated). While it is impossible to mitigate downside performance, our structure dictates we mitigate risk to the greatest extent possible.

Base Case

Even at the same investor IRR, BCP’s Performance-Based Structure increases net profit to investors because BCP does not charge fees, which lowers the overall project cost basis and increases cash flow.

Upside Case

In the event the deal outperforms, investors make a marginally higher return with a traditional structure. This begs the question: Is it worth the risk to invest with a sponsor that is incentivized by fees to do more deals?

Interested in learning more? Please click here to view an expanded exploration of BCP's Performance-Based Structure vs traditional waterfall structures.